Women often face special challenges when planning for retirement. For example, if they are the primary caregivers in their families, their careers may be interrupted to care for children or elderly parents, which means they may spend less time in the workforce and earn less money than men in the same age group. And even if they remain in the workforce, women still tend to earn less than men, on average. As a result, their retirement plan balances, Social Security benefits, and pension benefits are often lower.

Women often face special challenges when planning for retirement. For example, if they are the primary caregivers in their families, their careers may be interrupted to care for children or elderly parents, which means they may spend less time in the workforce and earn less money than men in the same age group. And even if they remain in the workforce, women still tend to earn less than men, on average. As a result, their retirement plan balances, Social Security benefits, and pension benefits are often lower.

In addition to earning less, women generally live longer than men, which means having to stretch potentially limited retirement savings and benefits over many years.

To help yourself or the women in your life or at work manage these financial challenges, consider the following tips.

If you haven't already done so, begin saving now

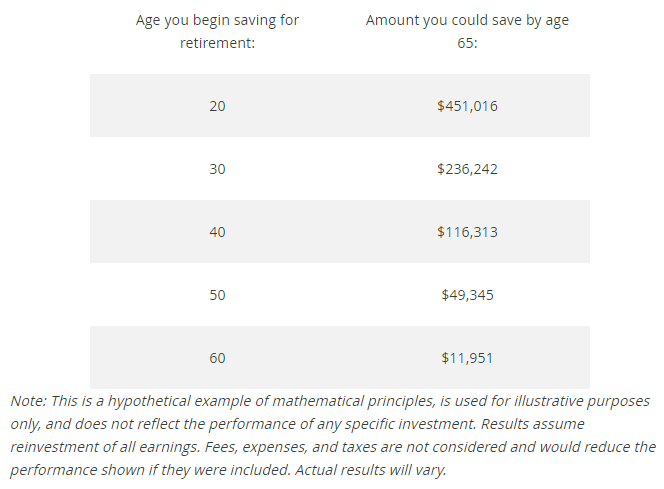

Start with a realistic assessment of how much you'll need to save. An online retirement savings goal-setting calculator can help. If the figure is substantial, don't be discouraged — the most important thing is to begin saving now. The chart below shows how just $2,000 invested annually at a 6% rate of return might grow over time:

Save as much as you can — you have many options

If you work outside of the home and your employer offers a retirement savings plan, such as a 401(k) or a 403(b), consider enrolling as soon as possible and contribute as much as you can. These plans make saving easier because your contributions are deducted directly from your pay, and some employers will even match a portion of your contribution.

If your employer offers a pension plan, find out how many years you'll need to work for the company before you are "vested in," or own, your pension benefits. Understanding this information can help you make an informed decision if you think you might need to leave your job at some point to care for family members. Keep in mind, too, that because your pension benefits will be based on your earnings and years of service, the longer you stay with one employer, the higher your pension is likely to be.

Most employer-sponsored plans allow you to choose from several investment options (typically mutual funds). If you have many years to invest or you're trying to make up for lost time, you may want to consider growth-oriented investments such as stocks and stock funds. Historically, stocks have outperformed bonds and short-term instruments over the long term, although past performance is no guarantee of future results. However, along with potentially higher returns, stocks carry more risk than less volatile investments. A good way to get detailed information about a mutual fund you're considering is to read the fund's prospectus, which can be obtained from the fund company. It includes information about the fund's objectives, expenses, risks, and past returns. A financial professional can also help you evaluate your retirement plan options.*

Save for retirement — no matter what

Even if you're staying at home to care for family, you can — and should try to — save for retirement. If you're married, file your income taxes jointly, and otherwise qualify, you may open and contribute to a traditional or Roth IRA as long as your spouse has enough earned income to cover the contributions. Both types of IRAs allow you to make contributions of up to $6,000 in 2021 (unchanged from 2020), or, if less, 100% of taxable compensation. If you're age 50 or older, you're allowed to contribute even more — up to $7,000 in 2021 (unchanged from 2020).**

Plan for income in retirement

Do you worry about outliving your retirement income? Unfortunately, that's a realistic concern. At age 65, women can expect to live, on average, an additional 20.8 years. In fact, many women will live into their 90s. This means that women should generally plan for a retirement that will last at least 20 to 30 years.

Women should also consider the possibility of spending some of those years alone. According to recent statistics, 31% of women age 65 and older are widowed, 17% are divorced, and 34% live alone. For married women, the loss of a spouse can mean a significant decrease in retirement income from Social Security or pension benefits.

So what can you do to help ensure you'll have enough income to last throughout retirement? Here are some tips:

- Estimate how much income you'll need. Use your current expenses as a starting point, but note that your expenses may change by the time you retire. Work-based retirement plans often provide helpful tools to estimate your income.

- Find out how much you can expect to receive from Social Security, pension plans, and other sources. What benefits will you receive should you become widowed or divorced?

- Set a retirement savings goal that you can work toward, and keep track of your progress.

- Save regularly, save as much as you can, and then look for ways to save more — dedicate a portion of every raise, bonus, cash gift, or tax refund to your retirement savings.

- Consider how you can help protect yourself and your family from potentially substantial long-term care expenses. By planning ahead, you could help preserve your choices for care and may avoid becoming a burden on your family.

- Understand these important "don'ts"

- Don't avoid the planning process - Perhaps you're so wrapped up in balancing your responsibilities that you haven't given retirement planning much thought. That's understandable, but if you don't put retirement planning at the top of your to-do list, you risk shortchanging yourself later on. Staying focused on your goal of saving for a comfortable retirement is difficult, but if you put yourself first, it could pay off in the end.

- Don't rely on your spouse - Married or not, it's critical for women to take an active role in planning for retirement. Consider that you may be forced to make important financial decisions quickly during a period of crisis. Preparing for retirement — or any financial goal — with your spouse could help ensure that you're both well-informed when the time comes to make the critical choices.

- Don't prioritize your children's education over your retirement - Many well-intentioned parents put their own retirement savings on hold while they save for their children's college education. But if you do so, you're potentially sacrificing your own financial well-being. Your children have many options when it comes to financing college — loans, grants, and scholarships, for example — but there's no such thing as a retirement loan.

- Don't neglect to learn the basics of investing - If you're unfamiliar with common investment terms such as diversification, asset allocation, and compounding, you can broaden your knowledge in as little as a few minutes each day. A simple web search can reveal hundreds of educational articles and videos. And remember, you don't have to do it by yourself — a financial professional will be happy to work with you to set retirement goals and help you choose appropriate investments.

*Financial planning and investment advice are offered through Sentinel Pension Advisors, Inc. Sentinel Pension Advisors, Inc. is a SEC-registered investment advisor.

**Securities products and services are offered through Sentinel Securities, Inc. Member FINRA & SIPC.

Julie Doran Stewart, MBA, CPFA, AIF®, RPA, is Head of Retirement Plan Advisory at Sentinel Benefits & Financial Group and can be reached via email: [email protected].

Alan Pfeffer, QPA, AIF®, is a Senior Vice President at Sentinel Benefits & Financial Group.